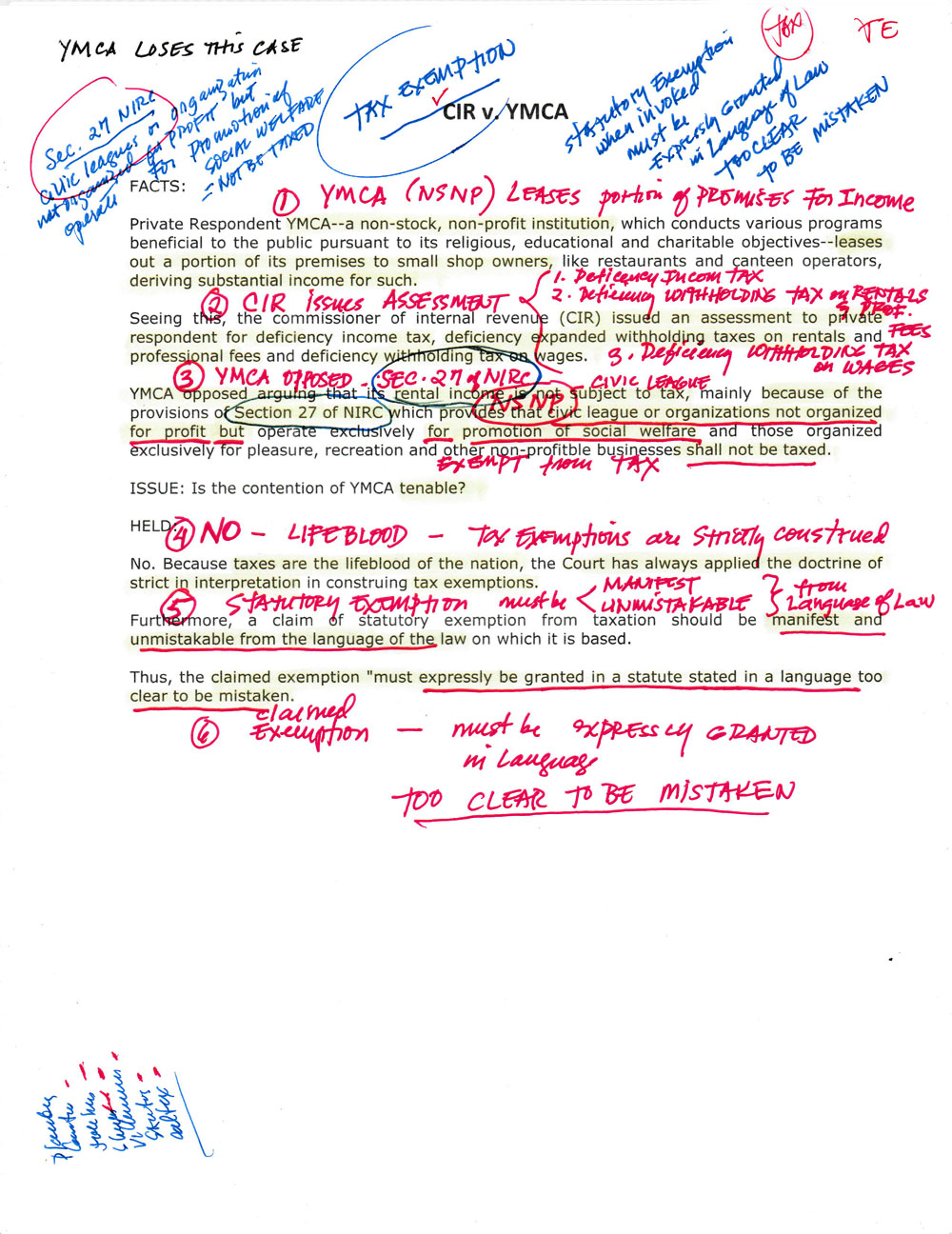

"Ey where's Dory??!!" Woops! somebody's excited to see 'Finding Dory' in the cinemas. After 13 years my goodness!! Finally!! We found Dory.

Try to check this out this is original. Manila International Airport Authority (MIAA) is the operator of the Ninoy International Airport (NAIA) formerly known as MIA (Manila International Airport) located at Paranaque City of course.

Try to check this out this is original. Manila International Airport Authority (MIAA) is the operator of the Ninoy International Airport (NAIA) formerly known as MIA (Manila International Airport) located at Paranaque City of course.

I wonder why its name was changed in the first place when MIA has more of a universal touch to it. Well now that President Duterte is taking over, and obviously we can sense that he is allergic to anything Liberal Party, I wonder if he would revert back NAIA's name to MIA. Well I hope he does. NAIA sounds like something that is wanting to be inclusive but by it sound still is exclusive.

Thing is.. I wonder how would we refer to it. "Ah.. lets meet at the MIA formerly know as NAIA which was formerly know as MIA". Geez funny I remember this upperclassman friend of mine when I was still new in my previous law school. His name's Prince. So whenever I see him at the corridor or maybe introduce him to lady batchmates I always refer to him (in a kidding mode) as "Prince!!.. formerly known as The Artist.. which was formerly known as Prince" LOL. (I'm reminded of Prince.. God bless his soul) "Chip you suck!" The guy just laughs reaches out and tickles my tummy. Ah he's such a nice friend. Works at a big bank in Makati. The guy's a prince really. His car's really nice. And such a nice guy too. I always saw him as an upperclassman whose not puffed-up. Well anyway.

Thing is.. I wonder how would we refer to it. "Ah.. lets meet at the MIA formerly know as NAIA which was formerly know as MIA". Geez funny I remember this upperclassman friend of mine when I was still new in my previous law school. His name's Prince. So whenever I see him at the corridor or maybe introduce him to lady batchmates I always refer to him (in a kidding mode) as "Prince!!.. formerly known as The Artist.. which was formerly known as Prince" LOL. (I'm reminded of Prince.. God bless his soul) "Chip you suck!" The guy just laughs reaches out and tickles my tummy. Ah he's such a nice friend. Works at a big bank in Makati. The guy's a prince really. His car's really nice. And such a nice guy too. I always saw him as an upperclassman whose not puffed-up. Well anyway.

So what happened here was.. the Officers of Paranaque City sent notices to MIAA due to real estate tax delinquency. MIAA then settled some of the amount.

Now when MIAA failed to settle the entire amount, the officers of Paranaque city threatened to levy and subject to auction the land and buildings of MIAA, which they did.

MIAA then sought for a Temporary Restraining Order (TRO) from the CA but failed to do so within the 60 days reglementary period, so the petition was dismissed.

MIAA then sought for the TRO with the Supreme Court a day before the public auction, MIAA was granted with the TRO but unfortunately the TRO was received by the Paranaque City officers 3 hours after the public auction. See what I told you? See how original this case was? I mean what on earth was MIAA doing?? Talk about all the right moves.

MIAA claims that although the charter provides that the title of the land and building are with MIAA still the ownership is with the Republic of the Philippines. MIAA also contends that it is an instrumentality of the government and as such exempted from real estate tax. So in other words, MIAA's bone of contention and defense lie solely on the principle that the land and buildings of MIAA are of public dominion and therefore cannot be subjected to levy and auction sale.

Let's see if it will hold.

On the other hand, the officers of Paranaque City claim that MIAA is a GOCC (government owned and controlled corporation) therefore not exempted to real estate tax.

ISSUE:

Whether or not:

1. MIAA is an instrumentality of the government and not a government owned and controlled corporation and as such exempted from tax.

2. The land and buildings of MIAA are part of the public dominion and thus cannot be the subject of levy and auction sale.

RULING:

1. Under the Local government code, (GOCCs) government owned and controlled corporation are NOT exempted from real estate tax.

MIAA is not a government owned and controlled corporation, for to become one MIAA should either be a stock or non stock corporation. MIAA is not a stock corporation for its capital is not divided into shares. It is not a non stock corporation since it has no members.

MIAA is an instrumentality of the government vested with corporate powers and government functions. Under the civil code, property may either be under public dominion or private ownership. Those under public dominion are owned by the State and are utilized for public use, public service and for the development of national wealth. When properties under public dominion cease to be for public use and service, they form part of the patrimonial property of the State.

2. The court held that the land and buildings of MIAA are part of the public dominion. Since the airport is devoted for public use, for the domestic and international travel and transportation. Even if MIAA charge fees, this is for support of its operation and for regulation and does not change the character of the land and buildings of MIAA as part of the public dominion.

As part of the public dominion the land and buildings of MIAA are outside the commerce of man. To subject them to levy and public auction is contrary to public policy. Unless the President issues a proclamation withdrawing the airport land and buildings from public use, these properties remain to be of public dominion and are inalienable. As long as the land and buildings are for public use the ownership is with the Republic of the Philippines

MIAA wins this case. Well I guess it has after all the luxury to take lightly such period prescriptions in this case. It knew very well from the start its contentions will be very strong.